Fedwire

Since 1915, the Federal Reserve has operated a wire payment system, known today as Fedwire. A typical wire transfer was described in this way by Cleveland Fed President Wilbur Fulton in 1953:

Let's say a customer of a member bank in the [Cleveland] Fourth Federal Reserve District wants to get $5,000 to San Francisco, and fast, to complete a business deal. His bank would ask us to transfer the funds. We would deduct the $5,000 from the member bank's account with us and wire the San Francisco 'Fed' to credit it to the reserve account of the proper bank in that city, on behalf of the person or corporation designated. The whole transaction might take less than half an hour."

In addition to executing transfers on behalf of customers, banks use the wire system to make other interbank transfers, such as loans to other banks or to settle securities transactions. As indicated by President Fulton's description, wire transfers are generally used for time-sensitive payments, taking advantage of the immediate and final processing of each transaction through adjustments to banks' balances with Federal Reserve Banks. In addition, wire transfers are generally used for large-value payments. In 1953, the average size of a wire transfer was about $500,000. In 2022, the average was about $5.4 million.

The Fed's Mandate for Providing Wire Payment Services

Before the Federal Reserve System was established, payments of the kind described by President Fulton were less efficient or accessible. Because the US banking system was fragmented geographically, no single institution had national operations to act as an intermediary for payments. Long-distance payments could be subject to time delays and costs of physically moving currency or gold to settle inter-bank debts. With the advent of the Fed, inter-bank payments could be settled immediately using banks' balances with the Fed (Garbade and Silber, 1979).

Congress anticipated that Reserve Banks would transfer funds among each other to facilitate the movement of money around the country in section 16 of the Federal Reserve Act. As operations commenced in 1915, the Board quickly set up a system to settle these transfers known as the Gold Settlement Fund, renamed the Interdistrict Settlement Fund in 1935 (Smith, 1956: 12).

In addition to Fedwire, the Fed offers small-value payment services, including check processing, electronic ACH payments, as well as FedNow, an instant payment service that began operations in July 2023. Private-sector institutions also offer payment services, and Congress sought to encourage competition between the Fed and private-sector alternatives in the Monetary Control Act of 1980. Overall, in providing these payment services, the Fed has sought to foster the efficiency, accessibility, and integrity of the payment system (Board of Governors of the Federal Reserve, 2001).

Improvements to the Fed's Wire System Over Time

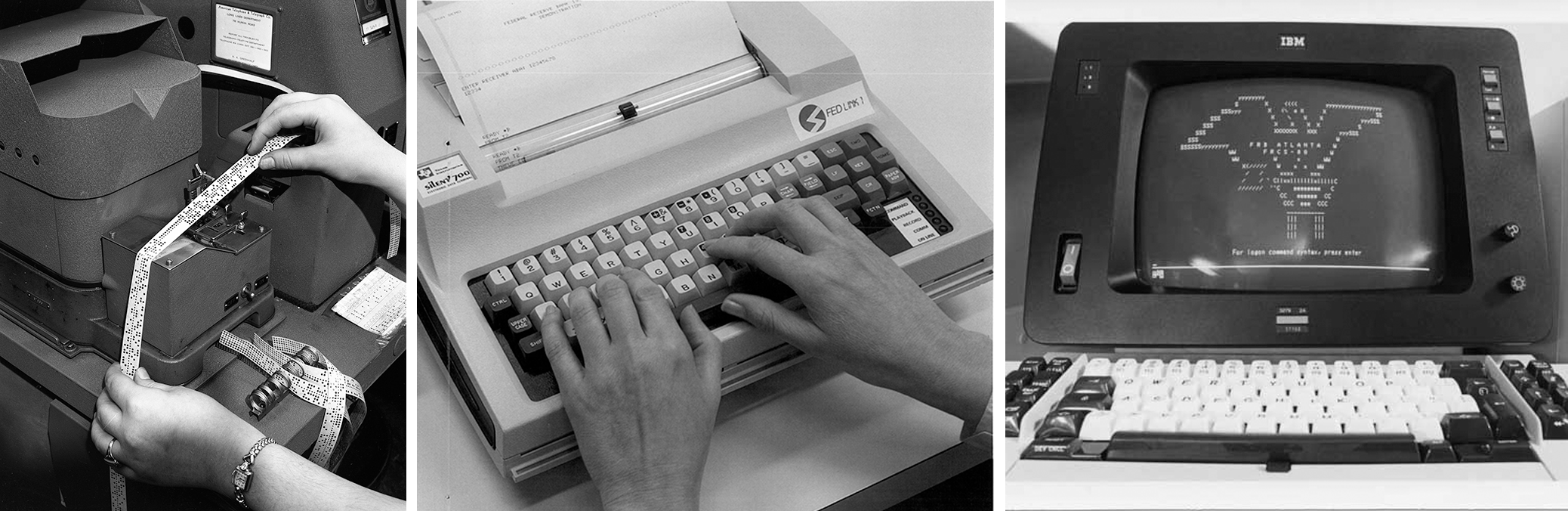

Telegraph wires were the original mode of communication for the Fed's large-value funds transfers. The telegraph system also carried other messages among the Reserve Banks, the Board, and parts of the federal government including the Treasury Department. The volume of communications was large enough for the Federal Reserve System to lease a dedicated telegraph system starting in 1918. Over time, this system has incorporated new technologies to boost the speed and capacity of funds transfers, reduce errors, and economize on costs:

- In the 1930s, operators began using teletype machines rather than Morse code to transmit messages.

- In the 1940s, relay equipment eliminated the need for re-typing of messages at key switching points in the communications system in Chicago and Washington, DC.

- In 1953, the telegraph system was overhauled and transmission became more automatic.

- In 1970, a second overhaul of the communication system supported full automation and computerized messages over telephone lines capable of high-speed data transmission. Reserve Banks began establishing computer-to-computer connections with member banks in their districts.

- In 1982 and 1996, successive overhauls establish the FRCS-80 and Fednet communication systems, respectively. Each overhaul introduced next generation software and hardware as computer technology improved.

- In the 2000s, Fedwire users transitioned from DOS-based access to web-based access.

- Beginning in 2014, Fedwire moved from a mainframe system to a "distributed" network of computers.1

At times, the need for additional capacity was acute. When the communication system was first overhauled in 1953, the volume of wire transactions was approaching 2 million annually and congestion was causing delays in the transmission of important messages. Computerization allowed the volume to climb from 7 million in 1970 to 52 million in 1980. By 1976-1977, 90 percent of wire transfers were initiated electronically through computer connections from banks to their local Reserve Banks, and the St. Louis Fed observed that the speed of transactions had fallen from "nearly an hour to only a few minutes." However, the communication system was again congested, "taxed to the point of bursting." (Stigum, 1983: 310). By 1998, the system saw 100 million wire transactions, and 200 million in 2022.

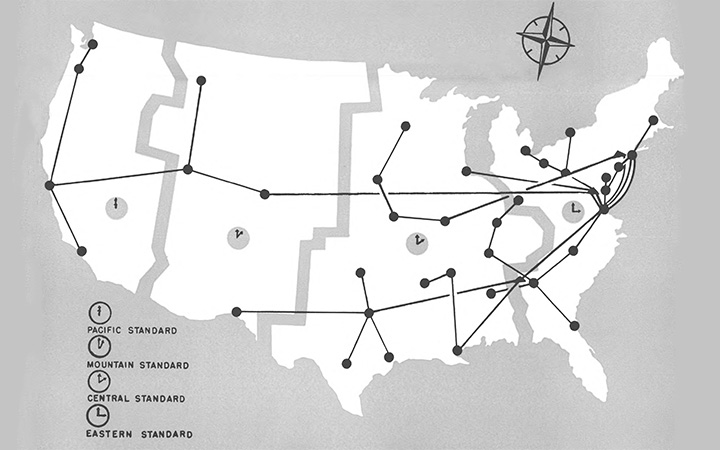

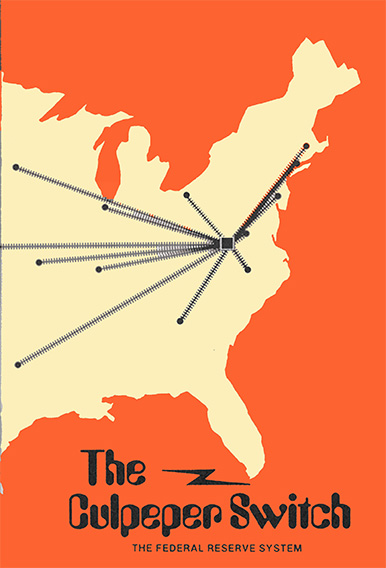

Federal Reserve officials saw the need to bolster Fedwire's resiliency. During the Cold War, for example, fears of nuclear attacks on large cities like Chicago or Washington, DC, motivated an overhaul in 1953 that eliminated the Fed's two telegraph relay centers in those cities in favor of routing all messages through Richmond (Robertson 1969). This routing function later moved to a new communications hub in a remote underground facility in Culpeper, Virginia, that began operations in 1970 (Federal Reserve Bank of Richmond 1970). After the 1982 overhaul, Culpeper continued as an operations center, but the hub was eliminated in favor of distributing computing power around the System to eliminate a single point of failure. With the end of the Cold War, the Culpeper facility was closed in the mid 1990s.

Each overhaul also brought some standardization to Fedwire operations nationally. Historically, though, Federal Reserve Banks often customized wire transfer protocols in their own district. Consistent wire transfer procedures became increasingly necessary in the 1980s and 1990s as large banks began to operate across multiple Fed districts amid the banking industry's consolidation. As part of the 1995 overhaul, Fedwire operations were standardized and unified under what is now known as Federal Reserve Financial Services, which runs Fedwire in a standardized way on behalf of all the Reserve Banks.

Fedwire in the Marketplace for Large-Value Payment Services

Bankwire and the Clearing House Interbank Payments System (CHIPS) are the two most significant privately run large-value payment systems that have operated in the US since the Fed's founding, both primarily serving large banks. A cooperative of large banks ran Bankwire from 1952 to 1986 (Smith 1956: 48-65). The New York Clearinghouse Association brought CHIPS online in 1970 (Lee 1977), and the system has been used especially to settle the dollar side of foreign exchange or other international transactions (Federal Reserve Bank of New York 1995: 9-10). Since the late 1980s, the volume of CHIPS transactions has averaged roughly two-thirds the volume of Fedwire transactions.2

Bankwire was, in part, a response to demand for additional wire transfer capacity for transactions by business or retail customers of large banks. Because telegraph lines limited the capacity of the Fed's communication network historically, until 1971 the Fed charged banks if they placed requests on behalf of customers, whereas banks could send payments for their own purposes for free if they were above $1,000. In 1971, with greater capacity from the upgraded communication system in place, the Fed changed its pricing to make all wire transfers above $1,000 free. The Board released a statement "Encouraging banks and their customers to make greater use of the expanded capabilities of the Federal Reserve wire transfer system." Executives at Bankwire, which charged per transaction, argued that the change in the Fed's pricing caused Bankwire to lose business (Romberg 1977, Watson 1986).

The Fed began charging for all Fedwire transactions in 1981 as required by the Monetary Control Act, which also broadened access to Fedwire, and other Fed payment services, beyond member banks to additional financial institutions. In setting prices, that act requires the Fed to "give due regard to competitive factors and the provision of an adequate level of such services nationwide." As observed by Fed Governor Lael Brainard in 2018, "Accessibility means serving more than 10,000 banks of varying sizes and missions that are in communities all around the country. It turns out no single private-sector provider of any U.S. payment system has ever achieved nationwide reach on its own..." (Brainard 2018).

Fedwire pricing has generally depended on the volume of a user's transactions and whether they are put in place online or in some other way, such as over the phone. In addition, since 1994 the Fed has charged fees for daylight overdrafts, which occur if a bank temporarily has a negative account balance with the Fed during the day, as a result of payments through Fedwire or other activity. These fees are part of a larger policy effort that the Fed initiated in 1985 to address the risks of large-dollar payments systems—both Fedwire and private systems—that could result, for example, from the failure of a payment system participant.

Fedwire Securities

In addition to transferring funds, Fedwire is also used to transfer securities issued by the US government and other issuers, as part of the Fed's role as the US government's fiscal agent. Short-term Treasury instruments were first transferred by the Fed's wire system in 1921, and longer-term Treasury bonds were in 1948. For example, if a bank in San Francisco sold a short-term Treasury certificate to a dealer in New York, instead of physically sending the paper securities, the San Francisco bank would simply deliver the paper securities to the San Francisco Federal Reserve Bank, which would communicate over the telegraph system with the New York Federal Reserve Bank to deliver a like amount to the dealer in New York (Garbade, 2012: 195). The ability to transfer bonds by wire broadened the market for Treasury securities out of major cities and helped eliminate small differentials in prices that once existed across cities (Smith 1956).

By the 1960s, paper records had become very cumbersome as a result of higher postwar trading volumes. In addition, the occasional loss of paper records increased the salience of their risks. The US Treasury and the Fed began working on the legal and practical aspects of transitioning to book-entry securities that are purely electronic records. The US Treasury gradually eliminated paper certificates over the next two decades, and ceased issuing them altogether in 1986 (Garbade, 2021).

Conclusion

The Fed's wire transfer system has moved from telegraph lines to high-speed data networks, leading to massive increases in speed, capacity, and efficiency. Amidst this change in technology, the basic vital function of Fedwire remains the same: to provide financial institutions with the means to instantly settle large-value transfers using their balances at their Federal Reserve Banks. A number of policy concerns have shaped the Federal Reserve's provision of this service over time, including ensuring the resiliency of the financial system to interruptions, such as Cold War fears or financial institution failures, and ensuring a competitive, efficient, and accessible payment system.

Endnotes

- 1 Smith 1956 describes the changes up to the early 1950s. Board of Governors 1976 provides an historical overview up to 1976. For additional information see Federal Reserve Bank of Cleveland (1953); Federal Reserve Bank of Richmond (1953); Federal Reserve Bank of Richmond (1970); Sherrill (1971). Board of Governors (1981); Board of Governors (1996); Federal Reserve Bank of New York (1995: 36); Board of Governors Annual Report (2004), (2007), (2014).

- 2 See The Clearing House and "Fedwire® Funds Service - Annual Statistics."

Bibliography

Board of Governors of the Federal Reserve System. Annual Report 1996, 2004, 2007, 2014, and 2022.

Board of Governors of the Federal Reserve System. "Federal Reserve Operations in Payment Mechanism: A Summary." Federal Reserve Bulletin, June 1976: 481-489.

Board of Governors of the Federal Reserve System. "Federal Reserve and the Payments Systems. Upgrading Electronic Capabilities for the 1980s." Federal Reserve Bulletin, February 1981: 109-116.

Board of Governors of the Federal Reserve. "Federal Reserve's Key Policies for the Provision of Financial Services." 2001.

Brainard, Lael. "Delivering Fast Payments for All." Remarks at a Federal Reserve Bank of Kansas City Town Hall, August 5, 2019.

Federal Reserve Bank of Cleveland. Annual Report 1953 and 1977.

Federal Reserve Bank of New York. "Fedwire: The Federal Reserve Wire Transfer Service." Monograph prepared by the Payments System Studies Staff of the Research and Market Analysis Group. March 1995.

Federal Reserve Bank of New York. "Changes in Wire Transfer Charges and Procedures." Circular No. 9102, July 1, 1981.

Federal Reserve Bank of Richmond. "Switching Center." Annual Report 1953: 8-9

Federal Reserve Bank of Richmond. "The Federal Reserve's Communication Center and the Payments System." Monthly Review, May 1970, pp. 7-10.

Federal Reserve System. The Culpeper Switch. 1975

Garbade, Kenneth D. and William L. Silber. "The Payment System and Domestic Exchange Rates." Journal of Monetary Economics vol 5, no. 1, January 1979: 1-22.

Garbade, Kenneth D. Birth of a Market: The U. S. Treasury Securities Market from the Great War to the Great Depression. MIT Press, 2012.

Garbade, Kenneth D. After the Accord: A History of Federal Reserve Open Market Operations, the US Government Securities Market, and Treasury Debt Management from 1951 to 1979. Cambridge University Press, 2021.

Lee, John. Statement. Federal Reserve Services: Hearings Before the Committee on Banking, Housing, and Urban Affairs, United States Senate. 105th Congress, 1st Session, October 10 and 11, 1977, U.S. Government Printing Office, 1977.

Robertson, J. L. Remarks at the Dedication of the Communications and Records Center, Culpeper, VA. December 10, 1969.

Romberg, Bernhard H. Statement. Federal Reserve Services: Hearings Before the Committee on Banking, Housing, and Urban Affairs, United States Senate. 105th Congress, 1st Session, October 10 and 11, 1977, U.S. Government Printing Office, 1977.

Sherrill, William M. "Banking at the Crossroads: The Outlook for Change over the Coming Years." Remarks at the 1971 National Automation Conference, American Bankers Association May 3, 1971.

Smith, George C. "The Federal Reserve Leased Wire System: Its Origin, Purposes, and Functions." PhD dissertation (Rutgers University, 1956)

Stigum, Marcia. The Money Market. Dow Jones-Irwin, 1983.

Watson, J. W. Henry. "Fed Drives out Competitors in Bank Fund Transfers." Wall Street Journal. March 13, 1986, p. 30

Published August 28, 2023. Jonathan Rose contributed to this article. Please cite this essay as: Federal Reserve History. "Fedwire." August 28, 2023. See disclaimer and update policy.

facebook

facebook

email

email