Check Payments

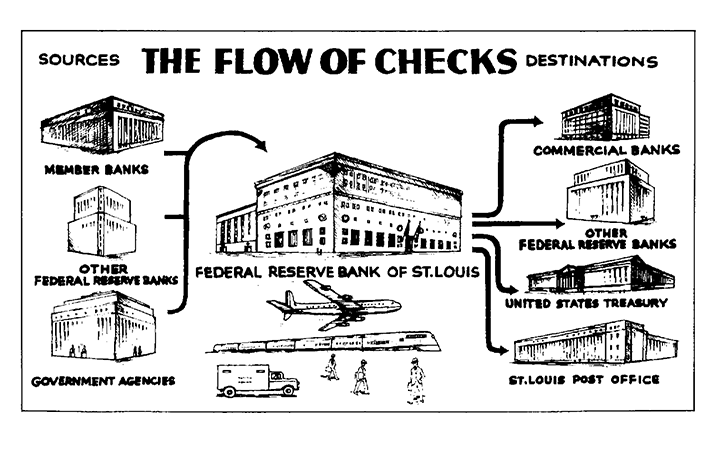

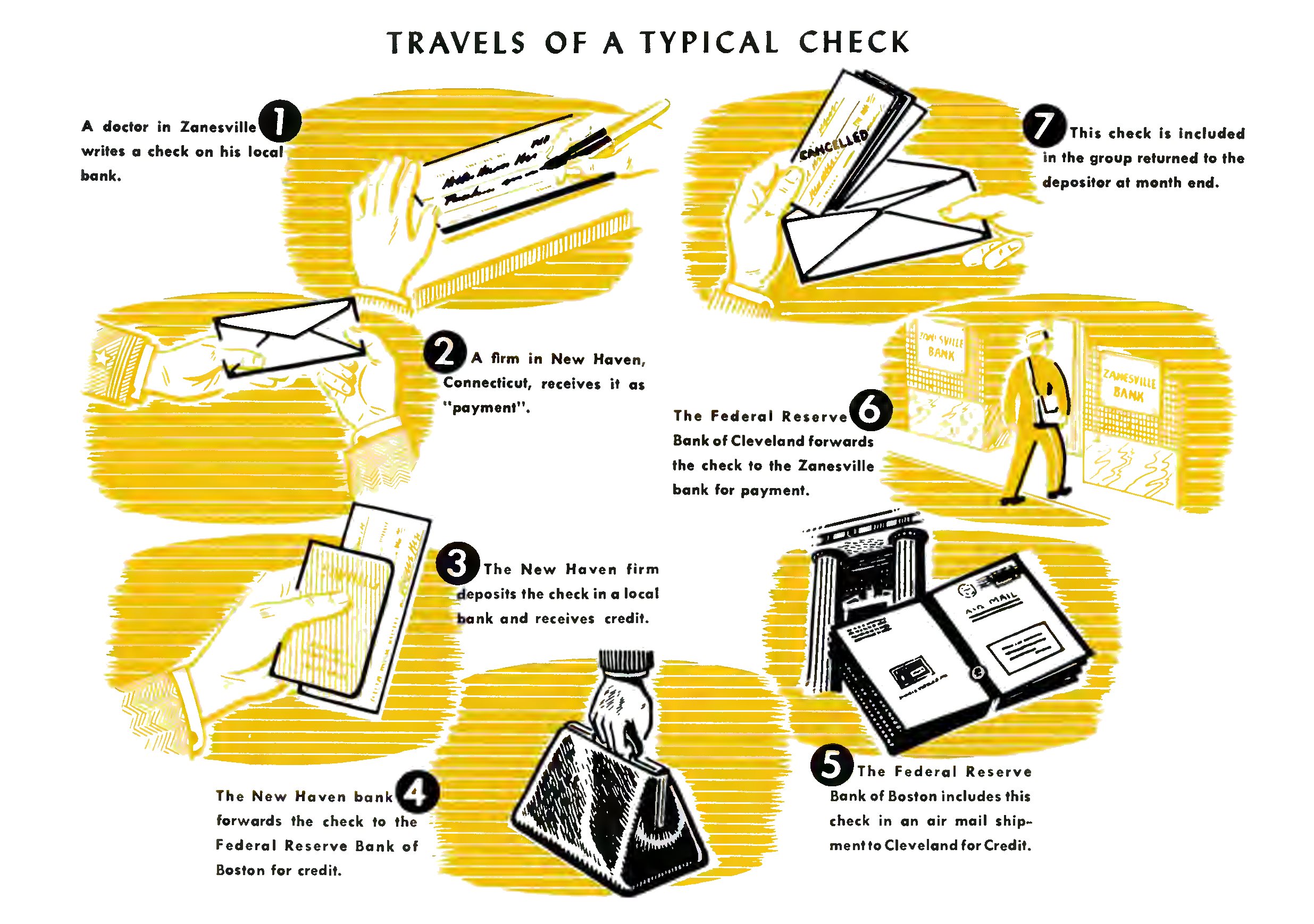

One of the responsibilities assigned to the Federal Reserve System upon its establishment was to improve the system for check payments in the United States. Contemporaries viewed the pre-Fed check payment system as inefficiently connecting the country's thousands of local banks. The Fed, by taking advantage of its nationwide reach, was uniquely positioned to streamline check collection—the process by which a deposited check is sent to the bank on which it is drawn to receive payment.

As a central bank providing payment services, the Fed pursues certain public policy goals, shaped by key pieces of legislation including the Federal Reserve Act and the Monetary Control Act of 1980. The Fed has sought to improve efficiency by increasing the speed of check payments and by promoting a competitive market for check clearing services. It has sought to ensure broad access to the check payment system by financial institutions of all sizes and locations. It has also sought to protect the safety of the check payment system in response to potential disruptions.

The Check Clearing System Before the Federal Reserve

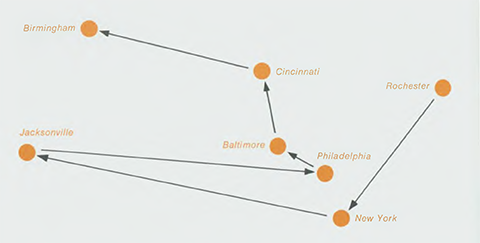

Checks were historically a popular means of payment in the United States in part because federal law discouraged banks from issuing their own paper currency (Quinn and Roberds 2008: 12). An elaborate check clearing system arose to distribute checks around the fragmented US banking system. Until the 1980s and 1990s, banks were highly restricted in their ability to branch across states or even within a state. As a result, it was often quite costly for a bank to collect a check directly from one of the tens of thousands of other banks in the country. If a bank was asked to settle a check through the mail, it might charge a fee to cover the cost. This practice was known as "non-par" banking because such banks did not pay out checks at the full face, or par value. Non-par banking was a subject of widespread criticism (Spahr 1926). Locally, such costs could be avoided by directly presenting a check to the bank on which it was drawn. Banks also exchanged checks locally through institutions known as clearinghouses. Otherwise, to avoid non-par costs, banks would send checks for collection through correspondent bank—banks that provided financial services to other banks. Correspondents were able to reduce costs because they bundled checks in with other mail they sent and the other services they provided. The correspondent process sometimes resulted in what was known as the "circuitous routing" problem in which a check wound its way through a series of banks based on their correspondent relationships. For example, Fed Governor William Harding recalled

"an instance where a national bank in Rochester, New York, sent a check drawn on a bank in North Birmingham, Alabama, to a correspondent bank in New York City, by which it was sent to a bank in Jacksonville, Florida, which sent it for collection to a bank in Philadelphia, which in turn sent it to a bank in Baltimore, which forward it to a bank in Cincinnati, which bank sent it to a bank in Birmingham, by which bank final collection was made." (Harding 1925: 51)

Historians have debated just how common this problem of circuitous check routing was (Chang, Danilevsky, Evans, and Garcia-Swartz 2008). Cases like the one described by Governor Harding were not the norm, but they do reveal that check collection was costly and that banks sometimes economized on cost at the expense of the time it took to route checks through correspondents (Lacker, Walker, and Weinberg 1999).

The Fed was able to cut through this web of correspondent relationships by using its direct connections to banks across the country. In an episode known as the "par clearing controversy," the Fed also sought to make par banking a national standard. In the Federal Reserve Act, Congress instructed Federal Reserve Banks to accept checks drawn on member banks at par. This represented a partial elimination of non-par banking, as the Act made no provision for what to do with checks drawn on banks that did not choose to join the Federal Reserve System. However, expanding on this mandate, the Federal Reserve System zealously sought to eliminate non-par banking altogether. If presented with a check drawn on a non-member bank, a Reserve Bank might employ an agent to travel to the bank, present the check in person, and demand full payment. The Fed's success was partial. Its actions reduced non-par banking but spurred litigation and new state laws that prevented its elimination; non-par banking declined but vestiges remained until the 1970s (Board of Governors 1976).

Increasing the Capacity of Check Processing

In the first few decades after the Fed's establishment, the basic technology of check processing remained largely the same. Check sorting continued to be largely manual, while mechanical adding machines were used for check "listing," in which the values of checks were added up by receiving and sending banks. Some efficiencies resulted from the standardization of the size and shape of checks, the adoption of routing codes for banks, and the creation of customer account numbers around mid-century (Federal Reserve Bank of Philadelphia 1960).

After WWII, a rapid rise in the volume of checks posed significant operational challenges for the Fed and the banking system. Once primarily used by businesses and wealthy individuals, checks became widely used for retail payments. Before the Great Depression, the number of checks handled by the Fed had peaked at about 900 million per year in 1929. Volumes reached 2 billion by 1946, doubled to 4 billion in 1960, doubled again to 8 billion in 1970, and doubled again to 16 billion in 1980.1

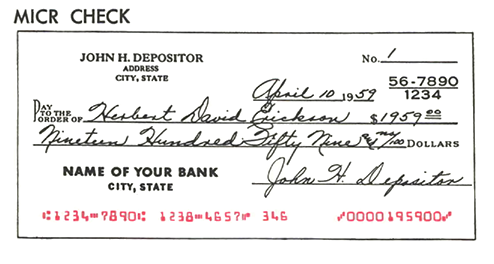

To handle the rising volumes of checks, the Federal Reserve System adopted new technologies. Mechanical "proofing" machines, adopted by Reserve Banks around 1950, allowed one operator to both sort and list checks at one machine, at a pace of 1,300 checks per hour. The adoption of magnetic ink in 1961 and 1962 significantly automated check processing by allowing computers to read all the necessary information from a check, save the amount. Magnetic ink boosted productivity to 33,000 checks per hour per employee initially; that pace went as high as 100,000 checks per hour eventually (Medley 2014). The banking industry ultimately preferred magnetic ink to alternatives such as bar codes or punch cards based on automation research in the 1950s. The Fed went from piloting the equipment in 1960 to requiring magnetic ink beginning in 1967.

Capturing check images is the most significant recent advance in the technology of check processing. Once, microfilm was commonly used to store images of checks for archival purposes (Connolly and Eisenmenger 2000). Banks began developing electronic check imaging technology in the late 1980s, with the goal of also "truncating" checks into an electronic form and obviating the need to move the paper check (Schram 2002). However, the basic technology took years to develop and legal obstacles were significant, as banks were not required to accept an electronic image of a check. Long-sought reform finally came with the passage of the Check Clearing for the 21st Century Act (known as Check 21 Act) in 2003, motivated in particular by the September 11, 2001, terrorist attacks that disrupted the transportation system, including the movement of physical checks. By 2010, the Fed System was receiving 98.4 percent of checks electronically.

For a time, the Fed and the banking system strained under the volume of checks that were "like a stream from a hydrant with a broken valve" (Federal Reserve Bank of Chicago 1952). About 7,500 people worked in check processing at the Fed at peak in 1974, accounting for 29 percent of all Federal Reserve Bank employment. Check volumes peaked in the early 1990s. Automated Clearing House payments, which the Fed began promoting in the 1970s as a substitute for paper checks, helped relieve some pressure on the check system, along with debit and credit cards. In 2022, checks accounted for about 5 percent of retail payment transactions, or 21 percent of the value of retail transactions (Federal Reserve System 2022).

Promoting Faster Payments

Accelerating check collection was a key motivation from the start for the Fed's entry into check payment services. In 1912, the average number of days it took to collect and settle a check from New York to other major cities, for example, was 5.3 days. That figure fell to 2.4 days on average in 1918 after the Fed's establishment. Some of this increased speed may have been due to the reduction of circuitous check routing. However, historians emphasize more the speed gains that came from settling checks instantly through Fedwire funds transfers rather than through the mail (James and Weiman 2010).

In 1952, the average speed of check collection was still about 2.3 days (Joint Committee 1954). The speed stayed roughly constant until 1971 when, in a "Statement of Policy on Payment Mechanism," the Board announced that "Increasing the speed and efficiency with which the rapidly mounting volume of checks is handled is becoming a matter of urgency" (Board of Governors 1971). Over the rest of the decade, the Fed constructed a number of regional check processing centers to limit the physical movement of checks, and by 1979 the average speed of check collection had fallen slightly to 1.9 days (Koch, Bennet, and Metzker 1982). At that point, the Fed was processing checks in 48 facilities, up from about 23 a decade earlier (Brundy, Humphrey, and Kwast 1979). More recently, with the Check 21 Act's elimination of the need to move paper checks, speeds have increased further, and today most checks are collected and settled in one business day. Today the Fed processes checks in one location, at the Atlanta Fed.

One factor slowing down check collection was the practice of remote disbursement. This practice involved corporate customers writing checks out of accounts in banks in remote areas, such as in rural areas far from major airports. The incentive for this practice stemmed from the ability of these customers to earn interest until the check was collected, known as check float. In 1979, the Fed called on banks to eliminate such practices, and emphasized banks' public responsibility to not abuse the check collection system by offering services designed to delay settlement (Board of Governors 1979).

The speed of funds becoming available to the check recipient also depends on how long a bank places a hold on those funds in case the check writer turns out to have had insufficient funds. In 1987, in response to widespread frustration with lengthy check hold times that could stretch longer than ten days, Congress granted the Board of Governors authority to regulate these hold periods through the Expedited Funds Availability Act. Initial regulations generally limited those hold times to seven business days at the longest, for out-of-town checks. Today, generally a bank must make check payments available in full by the second business day. The Board also established rules to speed the return of unpaid checks.

Promoting Competition and Efficiency

In providing check collection services, the Fed has competed with local check clearinghouses and correspondent banks. Historically, smaller banks and banks located in rural areas tended to send a greater portion of their checks to the Fed, reflecting their limited access to clearinghouses and the infeasibility of directly presenting checks to other banks. Banks also tended to use the Fed for checks drawn on non-local banks. The Fed gained some market share in the 1970s after establishing regional check processing centers, largely at the expense of local clearinghouses (American Bankers Association 1984).

The most significant change to the Fed's role in the check payment system resulted from the Monetary Control Act (MCA) of 1980. The MCA reaffirmed that the Federal Reserve should promote an efficient nationwide payment system. To encourage competition between the Federal Reserve and private-sector providers of payment services, the MCA requires that the Fed charge for its payment services. Up to that point, check clearing had been offered at no explicit cost to member banks, though member banks were required to hold reserves with the Fed. The MCA also extended access to Fed payment services and reserve requirements to banks that were not members of the Federal Reserve System and to other depository institutions such as savings and loans. The implementation of the MCA led the Fed to lose some share of the check clearing market over the 1980s (Summers and Gilbert 1996).

As the historic fragmentation of the banking system declined with the elimination of branching restrictions in the 1980s and 1990s, the original motivation for the Fed's entry into check payments in the early 20th century became less salient. In 1996, Fed Chairman Greenspan appointed a commission, led by Vice Chair Rivlin, to re-examine with fresh eyes what role the Fed should have in retail payments. The Commission's report concluded that the Fed should remain provider of both check and ACH services. It viewed withdrawal by the Fed from payments services as potentially reducing competition, given fixed costs of operating a payment network and the benefits of all participants being on a single network. The Commission was also concerned that reduced competition could make the payment system less resilient and reduce smaller banks' access to the payment system. Therefore, in envisioning the Fed's continued involvement in retail payment services, the Commission re-emphasized the public policy goals the Fed has had as a central bank providing payment services, including efficiency, safety, and accessibility (Committee on the Federal Reserve in the Payment Mechanism 1998).

Endnotes

- 1 These figures are taken from the Annual Reports of the Board of Governors of the Federal Reserve System.

References

American Bankers Association. "A Quantitative Description of the Check Collection System." 1981.

Board of Governors of the Federal Reserve System. "Statement of Policy on Payments Mechanism." Federal Reserve Bulletin, June 1971: 546.

Board of Governors of the Federal Reserve System. "Federal Reserve Operations in Payment Mechanisms: A Summary." Federal Reserve Bulletin, June 1976: 481-489.

Board of Governors of the Federal Reserve System. "Report on Remote Disbursement." Federal Reserve Bulletin, February 1979: 140.

Brundy, James M., David B. Humphrey, and Myron L. Kwast. "Check Processing at Federal Reserve Offices." Federal Reserve Bulletin, February 1979: 97. Available on FRASER

Chang, Howard H., Marina Danilevsky, David S. Evans, and Daniel D. Garcia-Swartz. "The economics of market coordination for the pre-Fed check-clearing system: A peek into the Bloomington (IL) node." Explorations in Economic History, 45(4), September 2008: 445-461.

Committee on the Federal Reserve in the Payments Mechanism. "The Federal Reserve in the Payments Mechanism." January 1998.

Connolly, Paul M., and Robert W. Eisenmenger. "The Role of the Federal Reserve in the Payments System." Federal Reserve Bank of Boston; 1998, 2000.

Federal Reserve Bank of Chicago. Annual Report 1952.

Federal Reserve Bank of Philadelphia. "How Banking Tames its Paper Tiger." Business Review. May 1960.

Federal Reserve Bank of Philadelphia. "How the Fed Helps Checks to "Hurry Back."" Business Review. June 1964.

Federal Reserve System. Federal Reserve Payments Study. 2022.

Harding, William. The Formative Period of the Federal Reserve System (During the World Crisis). Houghton Mifflin Company, 1925.

James, John A., and David F. Weiman. "From Drafts to Checks: The Evolution of Correspondent Banking Networks and the Formation of the Modern U.S. Payments system, 1850-1914." Journal of Money, Credit and Banking 42, 2010: 237-265.

Joint Committee on the Check Collection System. "Study of Check Collection System." American Bankers Association, Association of Reserve City Bankers, and Conference of Presidents of Federal Reserve Banks. June 15, 1954.

Lacker, Jeffrey M., Jeffrey D. Walker, and John A. Weinberg. "The Fed's Entry into Check Clearing Reconsidered." Federal Reserve Bank of Richmond Economic Quarterly, 85(2), 1999: 1-31.

Medley, Bill. "Highways of Commerce: Central Banking and the U.S. Payments System." Public Affairs Department of the Federal Reserve Bank of Kansas City. 2014.

Koch, Donald, Veronica M. Bennet, and Paul F. Metzker. "Lumbering at Top Speed: The Check Collection System, 1952-1979." Federal Reserve Bank of Atlanta Economic Review. March 1982.

Quinn, Stephen, and William Roberds. "The Evolution of the Check as a Means of Payment: A Historical Survey." Federal Reserve Bank of Atlanta Economic Review 93, no. 4, December 2008.

Schram, Lee. Testimony. H.R. 5414--The Check Clearing for the 21st Century Act: Hearing before the Subcommittee on Financial Institutions and Consumer Credit of the Committee on Financial Services, U.S. House of Representatives, 107th Congress, 2nd Session, September 25, 2002.

Spahr, Walter Earl. The Clearing and Collection of Checks. Bankers Publishing Company, 1926.

Summers, Bruce J., and R. Alton Gilbert. "Clearing and Settlement of U.S. Dollar Payments: Back to the Future?" Federal Reserve Bank of St. Louis Review, September/October 1996.

Published September 28, 2023. Jonathan Rose contributed to this article. Please cite this essay as: Federal Reserve History. "Check Payments." September 28, 2023. See disclaimer and update policy.

facebook

facebook

email

email